The 2019 North Carolina Water and Wastewater Rates Dashboard was deployed just over a month ago, marking another year in a long partnership between the Environmental Finance Center at UNC-Chapel Hill, the North Carolina League of Municipalities, and the North Carolina Division of Water Infrastructure. One of the benefits of such a long and successful partnership is the wealth of historic rates data.

The Rates Dashboard provides an up-to-date look at rates and financial sustainability indicators for utilities around the state, but it is merely a snapshot. By looking at trends in rates and demographic factors, such as income, the numbers and changes start to tell a story. A trends analysis was produced for a recent course on Water and Wastewater Finance at the UNC School of Government, looking at rates from 2009-2018, EPA SDWIS Service Population data from 2009-2018, and income, from US Census American Community Surveys, from 2007-2017. The figures below are adapted from that analysis. The analysis is restricted to utilities that have participated across all years and availability of data. By looking at the overall trend rather than the specific values, the resulting patterns can provide considerations for utilities across the state.

Trends in Monthly Water Bills

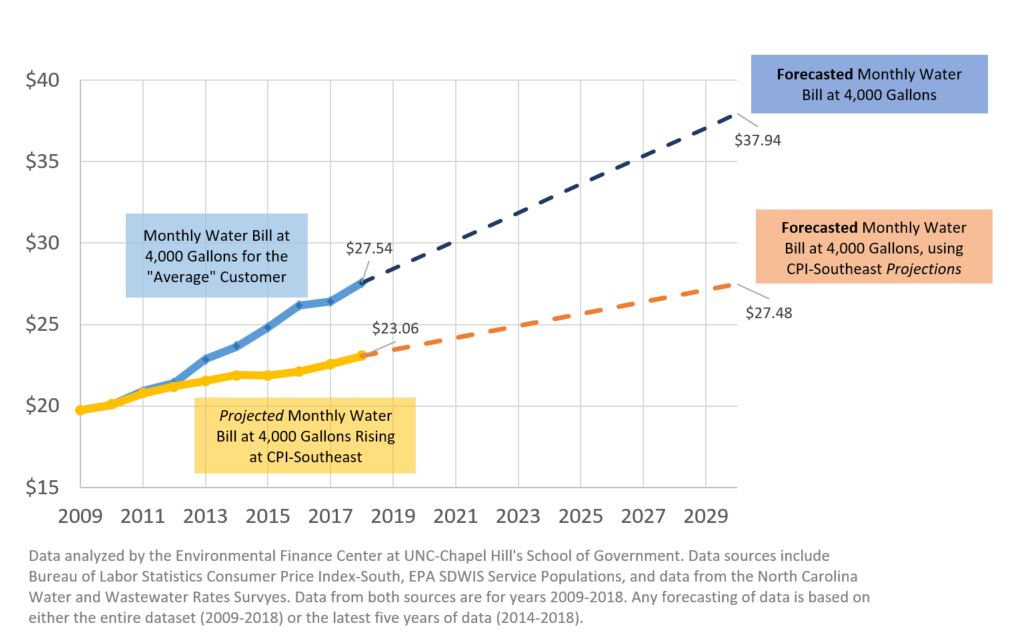

To conduct the analysis, we first looked at how the average residential water bill changed over time in North Carolina. This average bill is based on service populations and bills of each utility, and instead of showing the median water bill for utilities across the state, this analysis looks at bills for the median customer. For this analysis, this bill will be referred to as the monthly water bill at 4,000 gallons for the “average” customer.

The historic changes in this “average” customer bill were used to extrapolate what bills will look like in the future if they follow historic trends. These bills were then compared to what the bills would have been if they had been increased to match inflation using the Bureau of Labor Statistics Consumer Price Index (CPI) for the Southeast region of the US. The results are shown in Figure 1 below:

Figure 1: Average Monthly Customer Water Bill: Forecasted based on Bill Trends vs. CPI at 4,000 Gallons, 2009-2030 (n=226 utilities)

To orient the graph, The solid blue line is the “average” monthly water bill based on recent trends and from the EFC’s rates dataset and the yellow line shows what that monthly bill would have been if it was adjusted using CPI-Southeast. The dotted lines show the forecasted “average” customer monthly water bills from 2019-2030 based on the historical rates data and projected CPI-Southeast bill. Remember, the important thing is the trend…

So what are the key takeaways?

Since 2009, the average amount customers pay has risen significantly faster than inflation. We see the same trends exist among wastewater bills. This may be relatively old news for many; word has gotten around that infrastructure needs are upon us and the days of big grants and (artificially) low rates are on the way out. What is interesting is just how quickly the gap between what people are paying and inflation is growing, and how quickly it will continue to grow if rates continue to rise at this rate. This gap is reflective of a growing concern about the rise in bills relative to the rise in income. To assess what changes in income have looked like in NC, a similar trends analysis was conducted.

Trends in Income

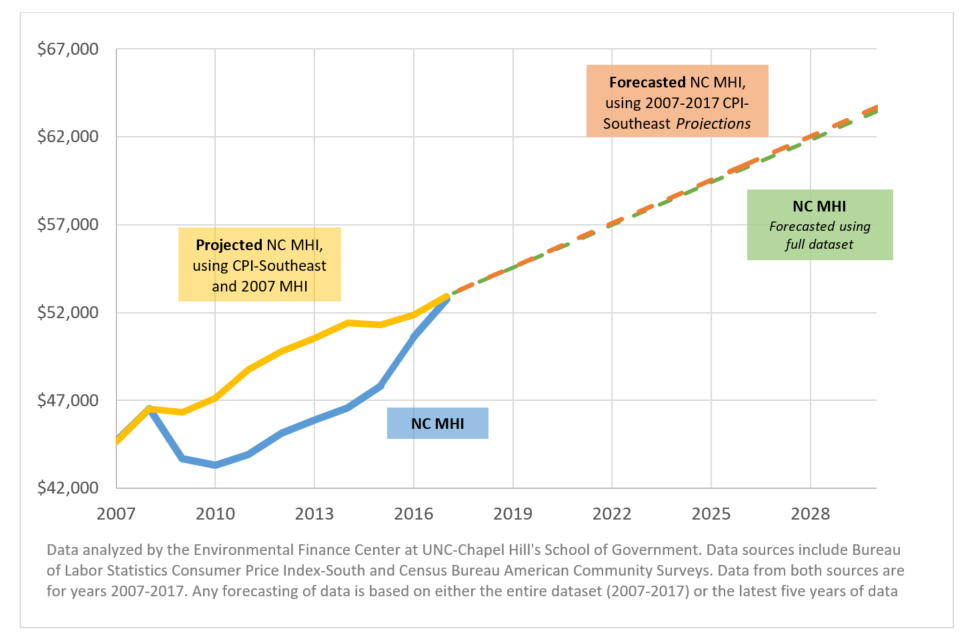

Considerable dialogue exists about the best way to assess water affordability. There are different metrics that provide insight into what affordability looks like for the most vulnerable customers, the median customer, and different customer classes. This post and the resulting figures are not about that share of income spent on water and wastewater service, but rather about trends in monthly bills and income, and what that might mean for customers their ability to pay for water services in the future. Figure 2 below shows how median household income (MHI) in North Carolina compares to inflation, 2007-2017, and forecasts to 2030 following the same methodology used for monthly water bills.

Figure 2: Trends and Forecasting, NC Median Household Income, 2007-2030

Key Takeaways of Trends in Income

North Carolina has experienced rapid growth in median household income over the past five years, but it has only just rebounded to the equivalent of 2007 when considering inflation. When using the entire dataset for forecasting, the inflated value and calculated value track together pretty closely. Inflation in the southeast region has grown at a slower rate over the past five years. Conversely, the MHI in North Carolina has grown rapidly in the last five years, resulting in an incredibly optimistic forecast that was excluded from this analysis.

What does it all mean?

While the median North Carolinians’ income has rebounded to keep up with inflation, it is unlikely that the rapid post-recession growth rates will continue. In addition, there is ample evidence that water bills will continue to rise at a rate that is faster than inflation. In short, the trends suggest that, in the future, affordability issues may begin to reach a greater proportion of customer bases and the lowest income customers may have even more trouble paying bills.

Again, this analysis looks at the state in aggregate and does not show anything about specific households or specific communities, which is essential to understanding and addressing affordability. What this analysis does show, however, is that there is a gap between the growth in income and the growth in bills that likely will pose future affordability challenges for more customers across the state.

Tools and Resources

Want to learn more about affordability for your customer base? Check out these EFC resources.